BLUF

The Iran war has not only disrupted global energy markets, it has also structurally reshaped them. Every day, Gulf oil and LNG exports are impeded, demand is driven higher, forcing states to seek alternative markets as strategic reserves dwindle. The United States has positioned itself as the primary supplier capable of filling this void. Russia, the world's third-largest LNG exporter, has faced compounding challenges brought on by Western sanctions, the destruction of the Nord Stream pipeline, and Ukraine’s escalating “kinetic sanctions” campaign against its refineries and shadow fleet. The UA’s withdrawal from OPEC on May 1st fractures the cartel that has constrained global supply for the last five decades, a major structural win for American energy interests. The United States is now positioned to supply up to 80 percent of Europe’s LNG by 2030, a monopoly it is actively leveraging as a diplomatic tool.

The structural advantages accruing to the United States are real but not irreversible. A swift resolution to the Iran conflict, a coordinated OPEC response, or a Chinese diplomatic intervention could each meaningfully erode the leverage described below.

Situation Overview

On February 28, 2026, U.S. and Israeli forces launched Operation Epic Fury against Iran, triggering the closure of the Strait of Hormuz and the worst energy supply disruption in decades. Not only has closure spiked prices, it has also begun to permanently redraw the map of global energy supply. The details of that disruption have been extensively documented elsewhere. This piece examines what comes next.

Russian Energy Disruptions

Russia is the world's current third-largest LNG exporter and a major oil producer. Energy plays a key role in its economy, accounting for about $120.1 billion or a little over 22 percent of the projected state income for 2026. This has made Russia’s oil and gas industry a prime target for Ukraine and the West.

Efforts to weaken Russian energy export capabilities have taken several forms.

Kinetic Sanctions

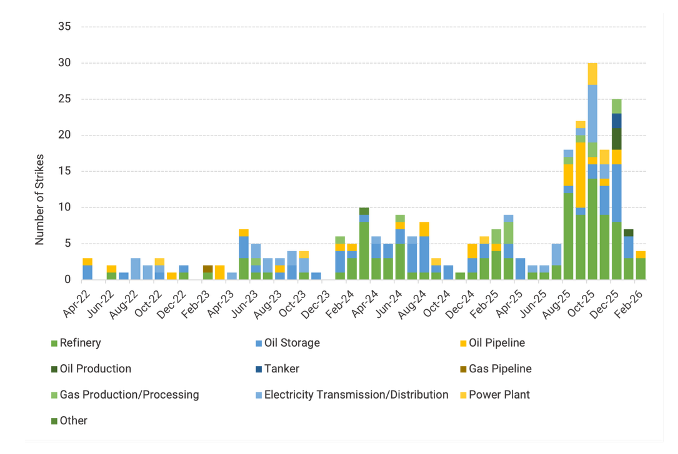

Ukraine has launched a full-scale onslaught against Russian energy infrastructure since the onset of the war. Over 272 discrete strike events have occurred or are suspected between April 2022 and February 2026.

The effectiveness and frequency of attacks have continued to increase over the last several months. In April 2026 alone, at least 21 confirmed strikes targeted Russian energy infrastructure, with at least nine of those specifically hitting processing facilities. Recent strikes hit targets over 1,500 kilometers from the Ukrainian border.

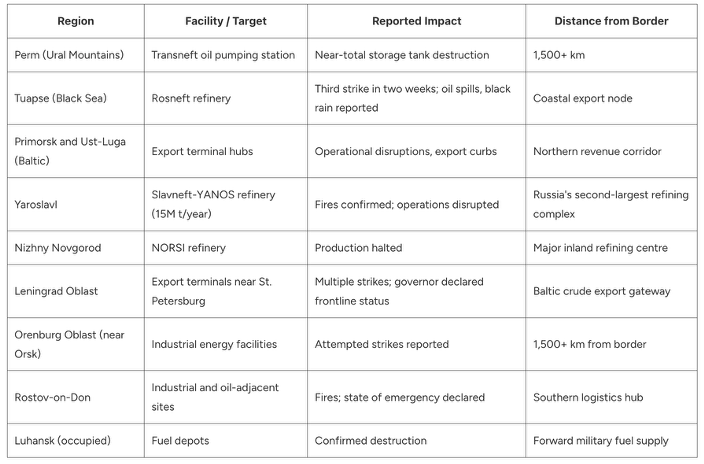

Overview of significant April attacks

The chief of the Security Service of Ukraine (SBU), Vasyl Malyuk, calls such targeting ‘kinetic sanctions,’ an apt name given the economic damage they have inflicted.

Cumulative infrastructure damage from this campaign has forced Russia to reduce crude oil output by an estimated 300,000 to 400,000 barrels per day. At prevailing Brent prices above $100 per barrel, a 350,000 barrel per day shortfall translates to roughly $12.8 billion in annualised revenue disruption. The price per barrel as of March 11th is $105.3, which raises this figure even higher. Russian refinery throughput has fallen to levels not recorded since 2009. This signals structural rather than temporary disruption.

Protection of these facilities has proved difficult. Russia has established a tight ring of air and missile defense systems around Moscow and appears reluctant to redeploy these assets. The aim is likely to keep the realities of the war distant from the regime, protecting Putin and the government and societal elites. This positioning leaves far-flung energy and military facilities or forces near the front more exposed. There is a possibility that some systems are repositioned following the completion of the May 9th Victory Day Parade, but a complete reprioritization is unlikely.

As long as Russian energy infrastructure remains unprotected, it will remain a high-priority target for Ukraine. Meaningful peace is a remote possibility for the foreseeable future. The US-brokered 3-day truce has already failed, with both sides claiming to have suffered casualties in drone and artillery strikes. A resumption of kinetic sanction activities is highly likely.

Economic Sanctions

Economic sanctions have proved a powerful weapon against Russia’s wartime economy. While the pricing repercussions of Operation Epic Fury have led Trump to ease US sanctions against Russia, Europe has not wavered in its position.

The EU passed the 20th sanctions package on April 23rd in coordination with the G7 and the Price Cap Coalition. The import ban comprehensively covers goods, technology, and services related to Russian LNG and crude oil projects, encompassing 90% of the EU’s current oil imports from Russia. What imports are allowed are severely price-capped, with seaborne crude oil fixed at a maximum price of 15% below market rate. This is the latest step in a series of increasingly strict sanctions as the West attempts to decouple from its reliance on Russian energy.

Current sanctions prohibit the import of seaborne crude oil and refined petroleum products from Russia. This is a significant blow as European markets make up about half of their export destinations. Liquefied petroleum gas (LPG) has also been banned, impacting annual imports worth roughly $1.2 billion, with existing contracts granted a maximum period of 12 months to completely phase out.

The Russian LNG sector has also been hit extremely hard, facing a complete ban from European markets as of January 2027 for long-term contracts. Short-term contracts have a six-month window to follow suit. Future investments in, and exports to, LNG projects under construction in Russia have been outlawed. So have LNG terminal services, allowing EU operators to terminate any long-term contracts with Russian operators.

Shadow Fleet Targeting

Russia has purchased an illicit “shadow fleet” of vessels estimated to range from 155 tankers and 435 total vessels, since sanctions limited oil exports in late 2022. Conservative estimates place the total size as high as 591 ships when support ships are included. These vessels are responsible for the transport of 65% of Russia’s seaborne oil trade, an estimated 3.7 million barrels per day. The revenue generated each year is estimated between $87 and $100 billion.

It is hard to understate the importance of this funding to Russia’s wartime economy. Shadow fleet revenue has matched, if not exceeded, the total value of economic and military assistance provided to Ukraine since the start of the war.

Legal measures against these vessels have proved difficult. The Russian shadow fleet is reported to employ a wide array of deceptive tactics to evade sanctions. These include ship-to-ship transfers, automatic identification system blackouts, falsifying positions, and the transmission of false data, including on ownership, vessel name, or even identity (IMO number). These efforts have impeded but not fully prevented sanction enforcement. Between December 25th and March 15th, at least 14 shadow fleet vessels were seized, detained or boarded by U.S., Indiana, and European Union authorities.

It is worth noting that the location of sanction enforcement has limitations. India accounts for 45 percent of Russian seaborne oil exports, and Turkey imports, on average, 425,000 barrels per day. These nations' close alliance with the United States effectively constrains Ukraine from attacking ships off either the Indian or Turkish coasts.

In tandem with its kinetic sanction efforts, Ukraine has launched a military campaign against Russia’s shadow fleet, often striking both vessels and refineries in a singular location.

A May 2nd drone strike set fires at Russia's largest oil exporting port on the Baltic Sea, the port of Primorsk, according to Russian regional Gov. Alexander Drozdenko. Zelenskyy claimed the attack destroyed several military and other targets, while also inflicting significant damage on oil port infrastructure. Ukrainian drones reportedly hit a Karakurt missile ship, a patrol boat, and a shadow fleet tanker, with an additional two shadow fleet tankers struck near the entrance of the Russian Black Sea port of Novorossiysk.

The reaction to such attacks has been strong. Russian seaborne crude exports via the Black Sea plunged 30%. One of Turkey’s largest tanker operators, responsible for managing several vessels sanctioned by Ukraine, announced that it will no longer transport Russian cargoes after one of its tankers suffered explosions off the coast of Senegal on 27 November. Insurance rates for ships that continue to trade in the Black Sea have increased by as much as 300% in early December 2025 and doubled again in January 2026.

The May 3rd attacks will likely further decrease future black sea shipping. Primorsk had already been targeted and struck by Ukraine multiple times in March, raising serious questions about Russia’s ability to protect its energy assets. If a known target can not be defended, future attacks will very likely continue.

Ukraine and the West can't prevent all Russian energy exports. However, a complete stoppage is not necessary. If Russia is viewed as an unreliable supplier, states will turn elsewhere for their energy needs, and/or Russia will be forced to undercut its pricing even further to retain its customers.

The Gulf Chokehold

Russia is not the only state currently struggling to export its energy.

The Strait of Hormuz closure and US naval blockade have significantly impacted Gulf states and Iranian oil exports, with no concrete diplomatic resolution in sight. For weeks, two competing blockades have left roughly 20% of the world's oil and LNG stranded and unable to reach its markets. An exact count of vessel transit is challenging to get, as ships sometimes fake or shut off their location signals to try to run the Strait. Global ship-tracking firm MarineTraffic indicates that at least six cargo ships have crossed the Strait of Hormuz since May 6th. Significantly, no tankers have been reported crossing in this window.

A renewal of shipping at scale within the next two months is highly unlikely. In fact, continued conflict appears imminent. Iranian leaders are claiming sovereignty over the Strait and seeking permanent control of maritime traffic through it. Weaponizing straight closure has been an incredibly effective tool for Iran, and control will not be relinquished lightly. Commitment is not merely rhetorical, as demonstrated by Tehran’s recent creation of the Persian Gulf Strait Authority (PGSA), an institution built to vet and tax vessels seeking passage through the Strait.

Washington has implemented a blockade of its own, redirecting and disabling vessels headed to or from Iranian ports. The United States and its allies have a vital interest in preventing Iran from holding this critical artery of global trade hostage. Allowing Iran to breach UNCLOS would set a dangerous precedent of non-enforcement and potentially inspire other states, such as China, to seize waterways of their own. Trump briefly launched Project Freedom in an attempt to escort stranded vessels through the Strait, but temporarily paused the operation not long afterwards to allegedly finalize a deal with Iran.

Without a drastic change, both states' contradictory interests render concessions unlikely, ensuring shipping through Hormuz remains limited.

Overland Routes

With the Strait effectively closed, Gulf states have primarily turned to pipelines for their energy exports. The feasibility and efficacy of this solution vary drastically by state.

Iraq’s pre-war crude exports (3.4 million barrels per day) went almost entirely through the southern port city of Basra and the Strait of Hormuz. While Iraq utilizes one recently reopened pipeline connecting oil fields in Kirkuk to Ceyhan in Turkey, flows only reached 250,000 barrels a day in March. This volume pales in comparison to what Iraq has lost.

Kuwait has fared even worse. It possesses no pipeline capacity, exporting the entirety of its 2 million daily pre-war barrels through Hormuz. Kuwait Petroleum Corporation declared force majeure in March, allowing it to temporarily suspend its delivery contract obligations. The company extended this cessation on April 20, saying it could not meet contractual obligations even if Hormuz reopened. Kuwait’s production base has suffered overwhelming damage, and ramping up production will take months.

Qatar is also completely reliant on the Strait for its energy exports. Its pre-war crude exports totaled around 0.6 million barrels per day, all transited through Hormuz. The biggest disruption, however, is Qatar's inability to trade liquid natural gas. Qatar supplies about 19% of the global LNG trade, making it the world's second-largest exporter. Ras Laffan’s 77 million tonne LNG capacity is the largest in the world, with no alternative to shipping this gas through Hormuz.

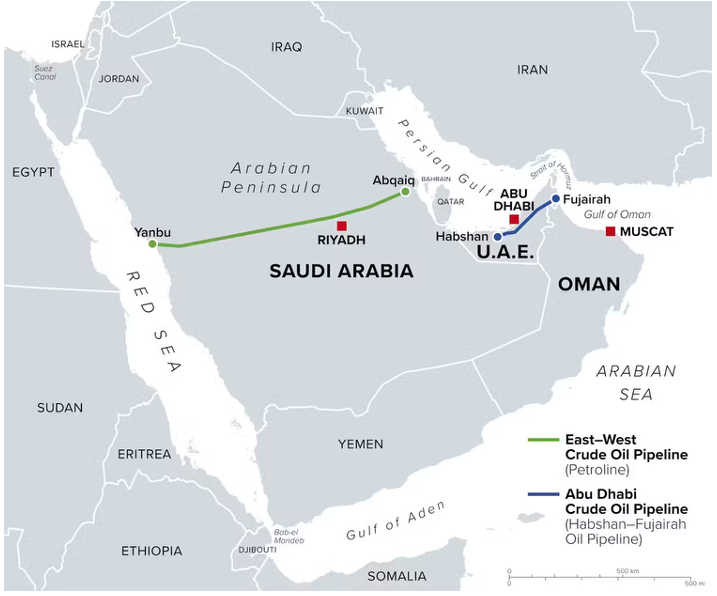

Saudi Arabia’s Petroline has become the state's lifeline for crude exports, with an alleged 7 million barrel emergency ceiling. However, this is an idealized projection. The loading terminals in the city of Yanbu were not designed for this volume, and the real volume is estimated to be lower. Oil bound for Europe is further constrained, having to cross Egypt via the Sumed pipeline, which has a capacity of just 2.5 million barrels per day. Although oil flows through this pipeline have surged by 150% since the start of the war, its comparatively small capacity remains a binding constraint on European supply.

The UAE’s Abu Dhabi Crude Oil Pipeline (Adcop) directly reaches the Gulf of Oman, making it the only major bypass to the Indian Ocean. Capacity is just under 2 million barrels per day, a sum notably under the Emirates' pre-war 3.4 million barrels per day.

The strategic importance of these pipelines has not gone unnoticed. Iran has targeted both the Petroline and Adcop pipelines and their surrounding infrastructure. March 3rd, 14th, and 16th Iranian strikes in Fujairah set storage tanks on fire and suspended loadings on the Adcrop. Weeks later, a drone attack on a Petroline pumping station eliminated 700,000 barrels a day of production. Saudi Aramco, the operator, had the line back at full capacity within three days. While rapid, this repair does not solve the targeting problem.

The scale and immobility of these pipelines and their supporting infrastructure leave them highly vulnerable to attack. Since the onset of Operation Epic Fury, Gulf states have become increasingly reliant on a small number of pipelines for the majority of their energy exports. At any point, Iran can resume its attacks, with the potential for devastating economic consequences. This is a serious threat with major leverage potential.

The UAE OPEC Exit

Energy disruption has a political element as well.

On April 28th, 2026, the United Arab Emirates announced its withdrawal from the Organization of the Petroleum Exporting Countries (OPEC), effective May 1st. The UAE was OPEC’s third-largest producer behind Saudi Arabia and Iraq. This withdrawal ends a fifty-eight-year membership in the cartel, dealing a significant symbolic blow to the economic alliance.

The motivation for withdrawal is multifaceted. UAE energy minister Suhail Al Mazrouei framed the decision as one of national interest, aligning with the country's long-term energy strategy. The UAE has the ambition to achieve 5 million barrels per day of capacity by 2027 and wants more freedom of action to pursue that goal. Al Mazrouei stated, "Our exit at this time is the right time for it, because it will have a minimum impact on the price and it will have a minimum impact on our friends at OPEC and OPEC+."

While Al Mazrouei claims the withdrawal “has nothing to do with any of our brothers or friends within the group,” the timing has a political element as well. Both the UAE and Saudi Arabia support a rapid diplomatic solution to Operation Epic Fury. The UAE, however, has taken substantial damage from Iranian attacks and is seeking guarantees that any agreement permanently limits Tehran’s ability to threaten Emirati security. Saudi Arabia, alongside Pakistan, Egypt, and Turkey, is perceived as overly willing to accept a less stringent settlement.

The UAE’s exit from OPEC draws it politically and economically closer to the US and represents a win for Donald Trump, who previously accused the organisation of “ripping off the rest of the world” by artificially inflating oil prices by holding back production. While Washington benefits greatly in the long term, American oil and gas producers will likely see some downturn in profits when the UAE supply hits the market. Notably, despite the potential for future defections, CFR analysts find it improbable that the Emirati decision will seriously undermine OPEC itself. The alliance will very likely survive, just in a weakened and less effective state.

Iran

While Iran is responsible for the Hormuz closure, its energy sector isn't faring much better than its OPEC peers.

April 14-15th, US Treasury Secretary Scott Bessent announced the Economic Fury campaign, a framework to use economic pressure to force Iranian cooperation. The operation targets Iran’s ability to generate, move, and repatriate funds across oil, banking, cryptocurrency, and covert trade networks.

Before the war, Iran exported roughly 2 million barrels of oil per day. Current exports have been halved, appearing closer to 1 million barrels daily. In total, 31 tankers laden with 53 million barrels of Iranian oil are trapped in the Gulf. Since April 13, the US Navy has intercepted and turned around 58 commercial ships that were either leaving or trying to enter Iranian ports. American forces have “disabled” four other ships that did not comply with American orders, as well as seized two Iranian tanker ships attempting to transit the Strait.

While Iran has an overland pipeline designed with a capacity of 1 million barrels per day, in practice, sanctions and unfinished terminal infrastructure have kept actual throughput at a fraction of design. Since the onset of Operation Epic Fury, only a single tanker (approximately two million barrels) has loaded at this pipeline. The same targeting vulnerabilities facing Gulf pipelines also apply to Iran, particularly given Trump's repeated rhetoric about attacking Iranian energy infrastructure. Maritime shipping remains the backbone of its energy exports.

The Defense Department estimates Iran has been denied nearly $5 billion in oil revenue because of the US blockade. Continued maritime closure will inflict an estimated $435 million per day in additional losses.

Further, with oil storage at Kharg Island nearing capacity and production shutdowns imminent, Iran has been forced to cut oil production by roughly 400,000 barrels per day, according to US Energy Secretary Chris Wright. Iran has begun to use older tankers as floating storage to delay overflow, but this is a temporary and imperfect solution.

Lack of oil storage is a universal issue. Dozens of refineries, storage facilities, and oil and gas fields in at least nine Gulf countries have been targeted in strikes. At least 10% of the world’s oil supply has been turned off. Restarting those operations will require not only safe passage through the Strait of Hormuz, but also inspecting pumps, replacing bespoke processing equipment, and recalling employees and ships that have scattered across the globe. Market analysts estimate it could take at least seven months for the world’s oil production to recover once the Strait of Hormuz reopens.

The Impact of Hormuz on US Gas and LNG

The nation best suited to benefit from these disruptions is the United States.

The closure of the Strait of Hormuz has had a proportionally small effect on American energy imports. The U.S. has emphasized domestic production, lowering its crude oil imports from countries in the Persian Gulf to the lowest level in nearly 40 years in 2024. Asian markets have been hit the hardest, encompassing an estimated 89% of the crude oil and condensate that moved through the Strait of Hormuz in the first half of 2025 (1H25).

American leadership has been seeking to capitalize on this position. Policies reflect deliberate, calibrated actions to entrench the U.S. position as the leading exporter amidst energy disruptions abroad. The Maritime Action Plan of February 2026 aims to usher in a “new Maritime Golden Age” by expanding commercial shipbuilding capacity, building a resilient workforce, and strengthening alliances. In March 2026, the Defense Production Act was invoked to force the restart of a Texas-based Sable Offshore Corp. pipeline in California, bypassing state environmental regulations. A subsequent April court ruling challenged the invocation, but the act signals a clear administration intent to maximize domestic production regardless of regulatory obstacles.

The January 3rd capture of former Venezuelan president Nicolás Maduro is the most drastic example of recent U.S. energy politics. American import and export capacity has skyrocketed with the renewal of U.S. extraction and processing of Venezuelan crude. Venezuela has the world's largest oil reserves, which the U.S. effectively absorbed when interim President Delcy Rodríguez opened these fields to U.S. investment. Venezuelan crude, often called a sour oil, is very heavy, thick, dark, and high in sulfur, making it much more difficult to process and lowering its market value. This is a non-issue for America as 70% of US refining capacity runs most efficiently with heavier crude. Notably, despite this efficiency, refining capacity has not yet been able to keep up with demand.

Shell has been pursuing extraction in the offshore natural gas field Dragon, straddling the maritime boundary between Venezuela and Trinidad and Tobago and containing an estimated 4.5 trillion cubic feet of recoverable natural gas. This will be a major asset once fully operational.

Competition

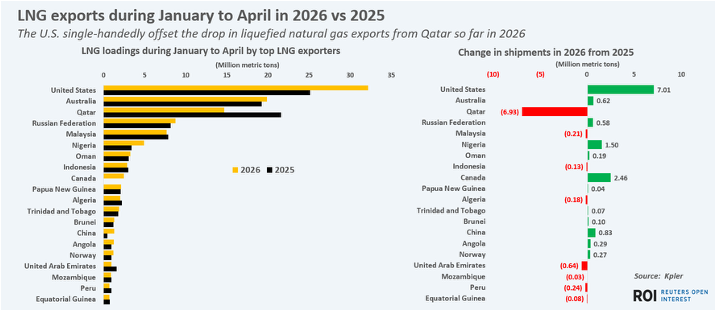

The closure of Hormuz has even further boosted U.S. LNG exports. With Qatari LNG offline, the United States has stepped in to fill the supply gap. America was already the world's largest LNG supplier before the onset of the Iranian war. The war has significantly increased the strength of this position. The U.S. exported a record high of roughly 32 million metric tons of LNG during the first four months of 2026. Despite the war, total supplies have remained at record highs.

The longer the Strait of Hormuz remains closed, the more entrenched the American energy monopoly becomes.

Damage to Qatari facilities was severe, eliminating 17% of Qatar's LNG export capacity for up to five years, according to the CEO of QatarEnergy. As long as peace between the United States and Iran remains uncertain, repairs to facilities will not be made, potentially denting Qatari production for years to come.

Australia, the world's next largest LNG exporter, was hit by a severe tropical cyclone, Narelle, on March 20. While the damage has since been recovered from, disruption is estimated at over 30 million tonnes a year of Australian LNG supply. Further, recent law states Australia’s east coast will have to set aside 20% of its gas exports to be sold to domestic users starting July next year. While Australia remains a top global LNG exporter, these factors have prevented it from seeing the same growth as the U.S.

Sanctions against Russian LNG prevent it from competing with the United States for the European market. Russia's share of EU imports of pipeline gas dropped from around 40% in 2021 to around 6% in 2025. Both LNG and pipeline gas imports from Russia have been prohibited as of 18 March 2026, and must be phased out by the end of 2027. While Russia still supplies Eastern markets, its reliability is impeded by sustained attacks.

Effects on Europe

The Hormuz closure has compounded European vulnerability. Without maritime transport, Gulf oil bound for Europe has to cross Egypt via the Sumed pipeline. Pipeline capacity is just 2.5 million barrels per day, a physical constraint on European supply unable to be overcome while the Strait remains closed.

European nations have been the top importers of U.S. LNG - accounting for around 72% of U.S. shipments so far in 2026. Distance from its Russian supplier had not quelled the European energy demand; it merely redirected it toward American sellers at American prices. The United States is positioned to supply up to 80 percent of Europe’s LNG by 2030

Europe has limited alternatives, a fact Trump has been quick to leverage. When negotiating a $750 billion energy deal with the EU, Trump’s ambassador to the bloc warned the arrangement must be accepted without amendments or the EU would risk losing “favourable” access to liquefied natural gas shipments from American exporters.

The arrangement is quite ironic. Over the past several months, the United States has been purchasing discounted Russian oil and petroleum products. Trump has temporarily waived some sanctions to permit such acquisitions to lessen the impact of Operation Epic Fury. The purchasing window is set to close on May 16th, with the potential to be renewed again. Simultaneously, the US is then processing and reselling refined American products to European partners at a premium.

American Maritime Positioning

As they grow in energy export dominance, the United States has been quietly consolidating its influence over the world's key maritime chokepoints through which this energy must flow.

Panama Canal

Since Blackstone acquired control of the Canal Zone in 2025, the Panama Canal has effectively been under the American sphere of influence. The Canal is the primary route for Eastern nations accessing Venezuelan crude exports, with China receiving over 75 percent. With the renewal of the United States refining Venezuelan crude, Beijing faces simultaneous disruption of both its Venezuelan supply chain and its transit access to it.

Strait of Gibraltar

On April 15th, the US and Morocco signed a new defense cooperation roadmap for the 2026-2036 period, enhancing American use of strategic bases in Morocco, freeing access to ports and airfields, and allowing for the prepositioning of material. This increased military presence between the United States and Morocco is not Washington punishing Spain for its recent actions. However, it does break Spanish hegemony as the almost exclusive interlocutor in the region. Without a Spanish response, Morocco will likely continue working with the United States to consolidate a dominant position in the Maghreb–Atlantic axis.

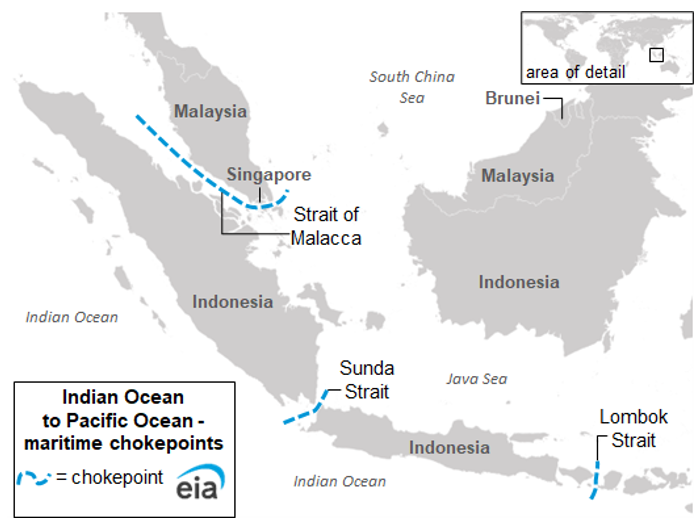

Strait of Malacca

The Strait of Malacca is the largest oil transit chokepoint in the world by volume, carrying the equivalent to 29% of global maritime oil flows. It is effectively unable to be bypassed, as the alternative transit must circumvent the entire Indonesian archipelago, adding thousands of nautical miles and many days to the journey.

A Major Defense Cooperation Partnership with Indonesia was signed on April 13, strengthening existing defense ties and giving US military aircraft expanded operational access to Indonesia's airspace through notification rather than individual authorization.

China accounted for 48 percent of import volumes passing through Malacca in the first half of 2025, encompassing the majority of Chinese energy imports. Closure of the Strait would be devastating for China and is a strategic non-allowance. A portion of this transit includes Russian shadow fleet vessels, of which the U.S. has already seized multiple.

Strait of Hormuz

The Strait of Hormuz is the most acute example of how control can be leveraged. The U.S. naval blockade was implemented in an attempt to extract Iranian concessions. It was utilized coercively when Trump suggested that the United States and Iran could work together to control the Strait of Hormuz and charge ships transiting it. Washington also demonstrated its willingness to use force by seizing and disabling vessels attempting to transit the Strait.

The United States does not have to formally close any of these straits to exercise leverage. They have the credible capacity to do so and a clear demonstrated willingness in Hormuz. China is the most exposed actor in this architecture, and the most likely target of escalating pressure.

Consequences for China

China is both the most exposed actor and likely target of American pressure on transit geography.

China accounts for approximately 90 percent of Iran's oil exports and was the largest destination for both Hormuz crude before the conflict. It also totaled almost one-third of LNG import volume that transited through the strait.

The simultaneous loss of Iranian and Gulf energy products, combined with reduced Russian supply, has placed Chinese strategic petroleum reserves under sustained pressure. China has prepared for energy disruptions, boasting an estimated 100-130-day storage capacity. While reserves won't be completely exhausted till June or July, they are drawing down and cannot be replenished at scale without access to Iranian, Gulf, or potentially Venezuelan supply. None of those sources is currently reliable.

For the United States, draining China’s oil reserves is a strategic goal. The Treasury Department has escalated pressure on Chinese "teapot" refineries, the independent processors responsible for purchasing the majority of Iranian oil. It called on US and international financial institutions to scrutinize transactions involving the independent refineries. Institutions deemed in violation will face sanctions. Hengli Petrochemical Refinery, one of Iran’s largest customers for crude oil and other petroleum products, has already been targeted.

The messaging is explicit: Chinese institutions' facilitation of the Iranian oil trade will be punished.

China's heavy dependence on the Strait of Malacca for its oil and LNG imports means that any deterioration in U.S.-China relations carries potential for a direct energy security dimension. Trump has previously indicated these corridor controls could be leveraged in negotiations. While direct action is unlikely, the administration's willingness to use economic instruments against allies and adversaries alike brings some credibility to these threats.

Leverage

The architecture described above is not exclusively directed at adversaries. Trump has demonstrated a consistent pattern of applying economic pressure to allied states, weaponizing tariffs, trade terms, and now energy access. The projected future U.S. monopoly of European LNG by 2030 is both a market forecast and a vulnerability assessment.

The waterway strategy attempts to extend that American leverage globally. Whether or not influence is leveraged remains to be determined. However, nations seeking a stable energy supply must prepare to increasingly navigate a system in which the United States wields its control over both energy supply and access terms.

Indicators to Watch

Qatari LNG Transit Through Hormuz

On Saturday, May 9th, a Qatari LNG tanker successfully transited the Strait of Hormuz en route to Pakistan, marking the first voyage of a Qatari LNG vessel through the Strait since the conflict started. A second tanker is currently transiting the Strait. These transits were approved by Iran as a confidence-building measure with Qatar and Pakistan, two leading mediators in the war.

While the renewal of transit at scale remains highly unlikely, there is a realistic possibility of Iran permitting future Qatari exports to Pakistan contingent on continued satisfaction with both states' role in negotiations. Watch whether selective permitting extends to China. An Iran-approved shipment to Beijing would force Washington to either enforce the blockade against its strategic ally Qatar or accept a concession and allow passage, which would majorly erode the blockade's credibility.

The War Powers Resolution

Trump has ignored the May 1st expiration of the War Powers Resolution, neither seeking congressional authorization nor submitting the written certification required to invoke the 30-day withdrawal extension. Operations simply continue. Enforcement of the withdrawal falls on Congress. A formal authorization vote, whether it's successful or failed, provides valuable information on where domestic support lies and the extent to which members of the legislature follow the party line.

Iranian Oil Storage

Kharg Island is nearing capacity, which has already forced Iran to cut oil production significantly. Once storage is full, refinement and extraction must slow to match whatever quantity is able to exit through the blockade. Public announcements or a sharp uptick in anchored vessels near the island could signal a shift in diplomatic or military posture as economic strain forces action.

Chinese Reserve Depletion

Chinese strategic reserves are limited and unable to be replenished in wartime circumstances. Aggressive Chinese spot market purchasing or a notable shift in accepted pricing likely signals that Beijing’s strategic reserves are weakening. A direct Chinese diplomatic intervention to reopen the Strait would similarly indicate reserve levels have crossed a strategically unacceptable threshold.

![]()

If you've read this far - you would be a perfect fit for the Intelligence Analyst Certification Course. Registrations for cohort 7 open 31st May. Hit the button below to get on the waitlist!

Responses